Global markets opened the week on a mixed note, with modest gains in stocks and bonds overshadowed by sharp volatility across energy, commodity and foreign exchange markets.

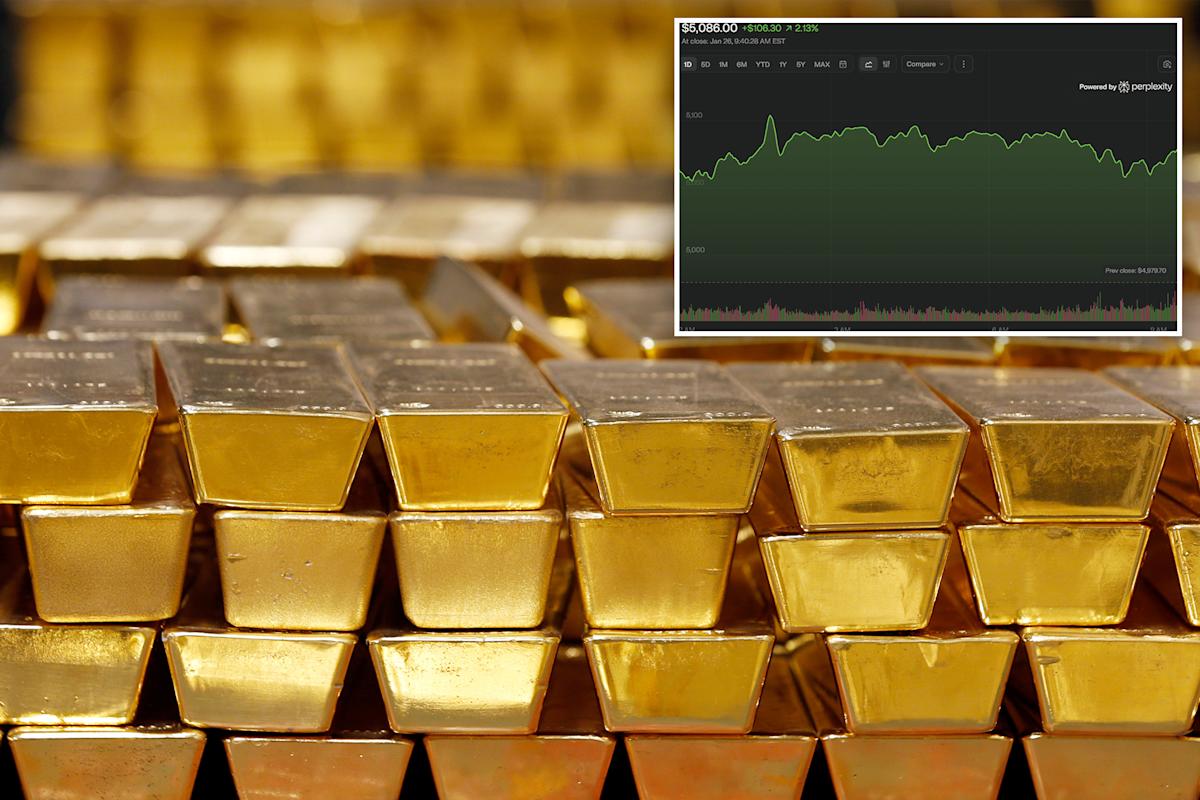

The US dollar slid to its lowest level since 2022, while gold surged past the $5,000 mark, reflecting heightened demand for safe-haven assets. Natural gas prices jumped nearly 30 per cent as a wave of cold weather swept across large parts of the United States, tightening supply expectations.

US equities extended their January rally, with the S&P 500 advancing further ahead of a crucial week of corporate earnings. Investors are bracing for high-stakes results from megacap companies, which have been major drivers of the market’s recent gains.

In the bond market, US Treasuries traded within a narrow range as expectations solidified that the Federal Reserve will pause further interest rate cuts in the near term, limiting directional moves in yields.

The greenback’s weakness was partly driven by speculation that the United States could coordinate with Japan on market intervention to help support the yen, which has been under sustained pressure.

After market close, shares of major US health insurers, including UnitedHealth Group Inc., CVS Health Corp. and Humana Inc., fell sharply following reports that the US government plans to keep payments to private Medicare plans flat next year, raising concerns over future profitability in the sector.

The earnings season is set to intensify this week, with companies representing about one-third of the S&P 500’s total market capitalisation scheduled to report results. Particular focus is on artificial intelligence-linked firms, which, after a rapid rally, are now under growing pressure to demonstrate that heavy capital expenditure commitments are translating into stronger earnings and long-term value.